Product feature update: Multiple bank accounts

Introduction

Investing decisions are often made in real moments when funds are available, when an opportunity fits your plan, or when timing feels right.

To make these moments easier, BondScanner now supports multiple bank accounts, allowing you to choose which account you want to invest from every time you place an order.

It’s a small change that brings meaningful flexibility to how you invest.

Why payment flexibility matters

Many investors don’t operate from just one bank account. You might manage savings across accounts for different purposes salary, investments, family expenses, or joint finances.

Until now, being restricted to a single bank account meant adjusting your plans around the app. But investing should adapt to how you manage money in real life not the other way around.

Flexibility at the payment stage removes friction and keeps the focus on the investment itself.

What’s new

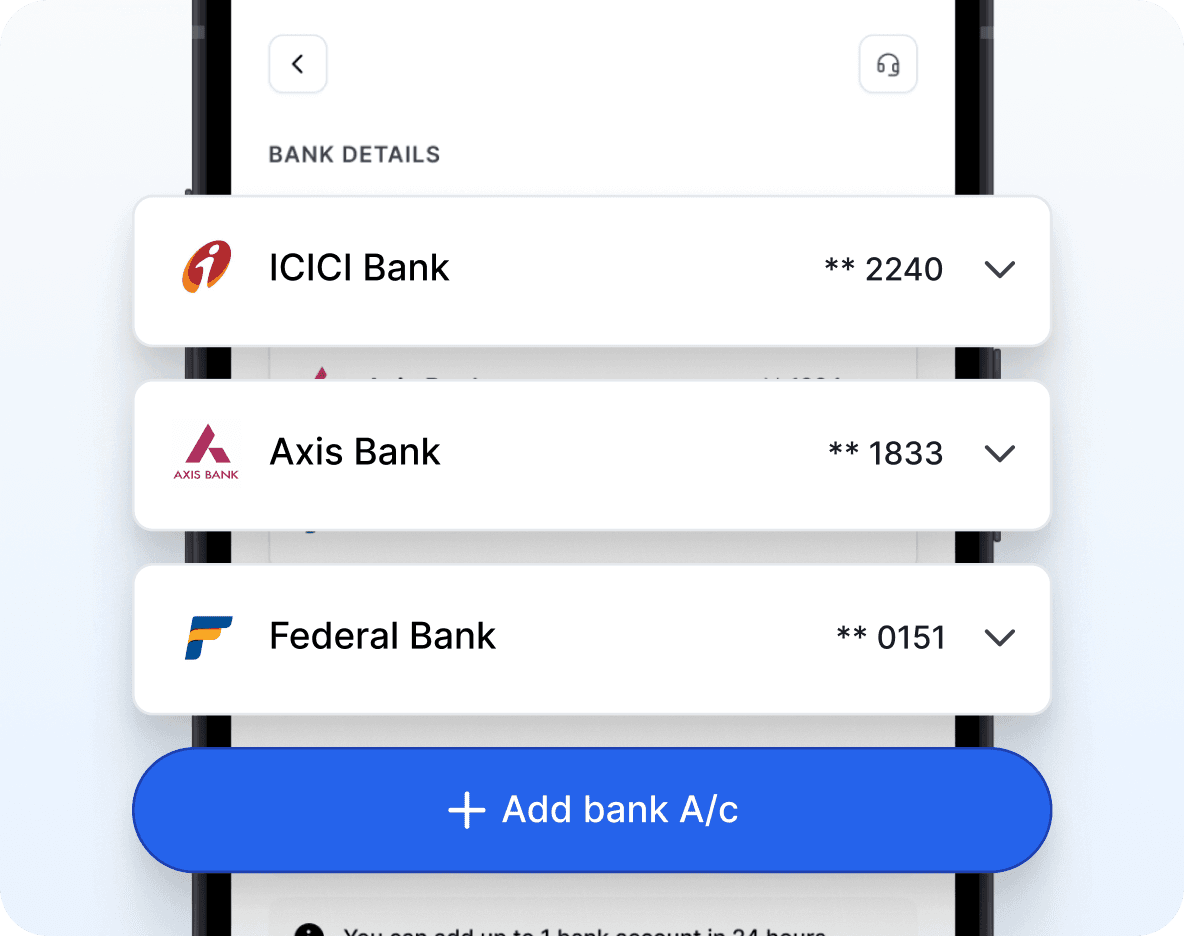

You can now add multiple bank accounts to your BondScanner profile.

When you’re investing, you’ll be able to select which bank account you want to use depending on what works best for you at that moment. There’s no need to switch defaults or update details repeatedly.

The choice is entirely yours, every time you invest.

How it works

Once additional bank accounts are added, they become available during the investment flow.

At the time of placing an order, you can simply select the account you want to invest from. The rest of the process remains unchanged quick, secure, and seamless.

This ensures that flexibility doesn’t come at the cost of simplicity.

Designed for real-life investing

This feature is designed around how people actually manage money.

Whether you’re separating long-term investments from daily expenses, using different accounts for different goals, or simply choosing the most convenient option at the time multiple bank accounts make investing feel more natural and less restrictive.

As portfolios grow and financial lives evolve, this flexibility becomes increasingly important.

Closing note

Good investing experiences remove unnecessary constraints.

By allowing you to add and use multiple bank accounts, we’re giving you more control over how you invest without adding complexity.

More thoughtful, real-world improvements coming soon.